Latest developments concerning your pension fund

A personal pension with solidarity |

In early April, Philips and the unions agreed on details of your future pension plan: the form that they have chosen is a solidarity based contribution plan. Philips Pensioenfonds will implement this plan for all pension beneficiaries, active members and policyholders of the Pension Fund. The solidarity based contribution plan is a form of pension designed by the legislature to make pensions more personal, with every member having their own pension savings, but also a shared buffer to prevent in case of financial setbacks.

We soon received some questions, for example “Will I be able to make my own investment decisions?” and “Do pension beneficiaries have a voice in the choices that are made?” Read on to find out more about the most important features of the new pension, as well as answers to these questions. I also explain what the role of Philips Pensioenfonds will be, now that we know what type of pension we will be administering for you.

|

|

|

|

Jasper Kemme

Managing Director

|

|

|

|

|

|

|

|

|

What does a solidarity defined contribution plan mean? |

The purpose of the new solidarity defined contribution plan is for members to have a personal pension, with protection in case of financial setbacks. In this plan there are some new elements, however not everything will change. So, what will stay the same, and what will be different? Watch the video for an explanation by actuary Pieter Vromen.

|

|

|

|

|

|

|

Pensions raised by the rate of wage inflation |

As we already informed you in late March, your accrued pension was raised by 4.0% on 1 April 2024. This increase is important, even if you are not retired yet: it helps your pension to retain its value until you start drawing it. “My pay rise under the CLA was 7% this year. Why hasn’t my pension gone up by the same rate?” was a frequently asked question.

|

|

|

|

Important: if your employment has ended and you are no longer actively accruing a pension with us, your pension was raised by the rate of price inflation. Click here to find out more

|

|

|

|

|

Poll: "I am pleased with the increase in my pension in 2024" |

|

|

|

|

|

|

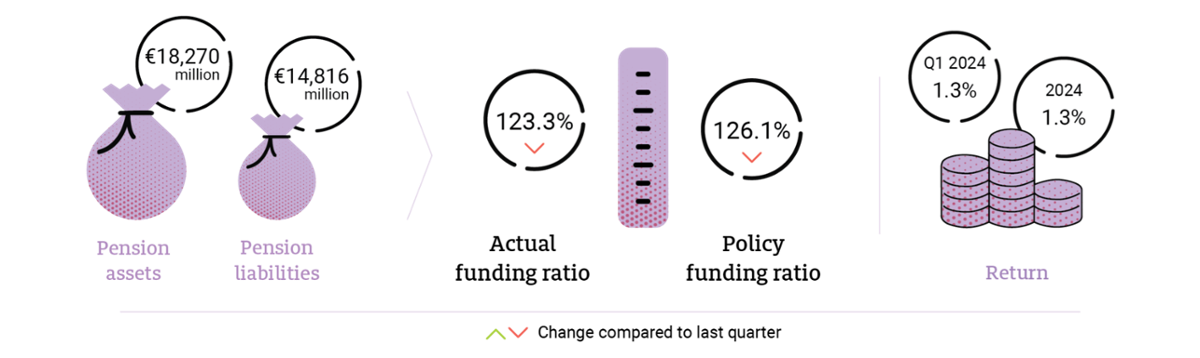

How is Philips Pensioenfonds doing? |

|

|

|

|

Have you just joined Philips Pensioenfonds? |

1. ...in MijnPPF, you can check your personal details and change the settings for language and communication methods. For us to send you information about your pension, for example, we need to have your correct home address and email address.

2. ...if you are living together without being married or in a civil partnership, you need to sign up your partner for a survivor’s pension. If you want to provide extra financial support in the event of your death, you have 3 months to take out the Anw shortfall insurance.

3. ...you can transfer the value of pensions that you accrued with previous employers to Philips Pensioenfonds.

|

|

|

|

|

|

|

"Can I get help with my pension options when I retire?" |

— A question that Ruben of our Service Desk is frequently asked —

|

|

|

|

|

"Yes, you can! You can set up an appointment for a video call or a face-to-face meeting in Amstelveen or Eindhoven. During this pension chat, we explain the pension plan, or discuss what options you can choose when you retire or how changes in your situation affect your pension, for example if you divorce or suffer a disability. Ask your question, and we will look at the possibilities in the Pension Planner."

|

|

|

|

|

|

|

|

Philips Pensioenfonds not on social media anymore |

|

|

|

We have decided to stop posting on social media. Our channel on X (what Twitter is now called) had very few followers. In our previous newsletter we asked whether you would be interested in reading our articles on LinkedIn. The feedback was that overall you have little interest in social media, and that you prefer to receive information about your pension in a newsletter, or in the online environment MijnPPF. With this in mind, we have decided to share information through those channels.

|

|

|

|

|

|

|

This newsletter is intended for members of Philips Pensioenfonds who have not yet retired. Visit our website for the newsletter for members who are drawing a pension

|

|

|

|

|

|

|

What do you think of this newsletter? |

|

|

|

|

|

|

|

|

|