Latest developments concerning your pension fund

Latest developments concerning your pension fund |

|

|

|

|

Details of the new pension plan agreed |

Your future pension has been discussed here many times already. Now, more details are known about how the future pension plan will work. Last spring, we announced that Philips had decided that it would be a solidarity-based contribution plan. Now Philips and the employee organisations have agreed on all the details of the new pension plan and recorded them in their ‘transition plan’. Also the the other employers whose pension plans we administer have adopted their transition plans. During the period ahead, we will not only review the transition plans to decide whether we are willing and able to carry them out, we will also start work on providing explanations.

In this newsletter, we start with the basics: after the switch to the new pension plan, you will have a personal pension capital instead of accruing a pension value. Visit our website to find out how this will affect you, with videos, FAQs and even a quiz to test how much you know. We will use the period ahead to highlight various topics relating to the details of the new pension plan. If you have any questions, please let us know, so that we can make sure that our information provides all the answers that our members need.

Jasper Kemme

Managing Director

|

|

|

|

|

New pension plan: did you know... |

- the transition plan includes calculations of how the new arrangements, in general terms, will impact the future pensions, assuming that our financial health remains strong?

|

- those calculations indicate that, immediately after we make the switch, each of our members is expected to have a higher pension than under the existing pension plan?

|

- pensions that our members are already drawing will have a high degree of protection against cuts: a reserve will be formed to supplement the pensions if the investment yields and other results fall short?

|

|

|

|

- besides benefits, the new pension plan also carries risks, as your pension will follow economic fluctuations more closely. This means that pensions that our members have not started drawing yet, might be lower than foreseen at this time.

|

| |

|

|

|

The pension plan in more detail |

The details of your future pension plan are set out in the transition plans of the employers for whom Philips Pensioenfonds executes the pension plan. Each transition plan includes a summary in which you can read what the agreements mean in broad terms. |

|

|

|

|

Switch to new pension plan scheduled for 1 January 2027 |

In slightly less than two years, all our members will fall under the new pension plan. The switch is scheduled for 1 January 2027. |

|

|

|

|

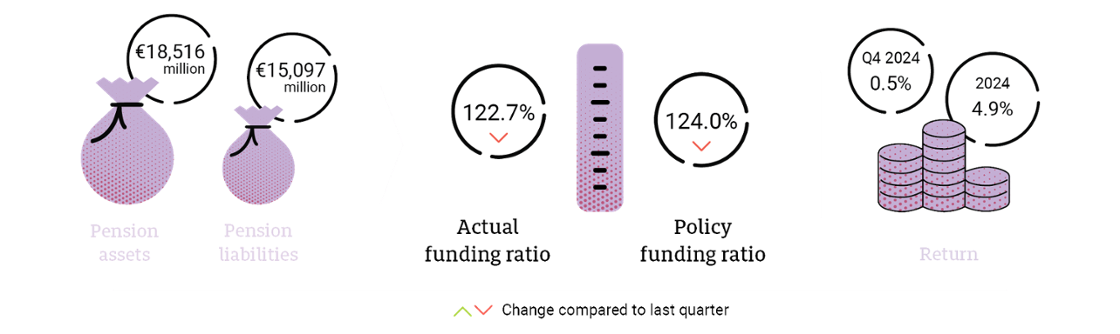

How is Philips Pensioenfonds doing? |

|

|

|

|

Indexation to be announced in March |

|

|

|

In March, the Board of Trustees will decide on your pension’s indexation for 2025. The regular annual indexation moment is 1 April; you will receive personalised information about the 2025 decision shortly before that date. |

|

|

| |

|

|

Poll: "I may decide for myself at what age to retire" |

|

|

| |

| |

|

|

“Retiring: before or after the switch to the new pension plan?”

|

— A question that Ruben of our Service Desk is frequently asked — |

|

|

|

|

The new pension rules will apply to everyone who is a member of Philips Pensioenfonds. In that respect, it does not matter whether you retire before the switch to the new pension plan, or after. If you are an active member when we make the switch (scheduled for 1 January 2027), however, you might be entitled to compensation, depending on your age: the compensation for active members who will suffer a disadvantage in their future pension accrual as a result of the new pension rules. |

| |

|

|

|

We recommend that you consider that compensation when you decide when to retire. You will be entitled to the compensation if you are an active member of Philips Pensioenfonds at the moment of the switch, and if your age is between 40 and 68 at that time. This includes if a disability renders you unable to work and we continue your pension accrual. |

|

|

| |

|

|

This newsletter is intended for members of Philips Pensioenfonds who have not yet retired. Visit our website for the Dutch version of this newsletter and for the newsletter for members who are drawing a pension. |

|

|

| |

|

|

What do you think of this newsletter? |

|

|

| |

| |

|

|

|