News about your new pension

How will the NexT Pension scheme affect you? |

|

|

|

|

Slowly but surely we are working towards personalising the information about your new pension system: the NexT Pension scheme. Until that time, we will try to give you an idea by explaining how the NexT Pension scheme will affect people like you. This newsletter has been put together specifically for members who are below the age of 55 and accrued a pension with us in the past.

Next week’s annual 3-day event the Pensioen3daagse will increase the country’s focus on the subject of pensions, so I believe that now is the perfect time to reach out to you. The question that you are probably most interested in is how the NexT Pension scheme will affect your own personal pension situation. We will not be able to share specific information about your personal situation until shortly before we switch to the NexT Pension scheme on 1 January 2027. For now, however, we can give you an idea of what to expect, and explain the most important matters that might be relevant in your situation. This newsletter is a key tool in these communications. Approximately midway through next year, further details about your new pension will be made available in MijnPPF. |

|

|

|

|

Anita Joosten

Managing Director |

|

|

|

| |

|

|

This is Karin. Karin is 44 and is not accruing a pension with us anymore. If, on 1 January 2027, you are like Karin – below the age of 55, with a pension from previous employment with Philips, Signify or Versuni – then your pension situation will resemble Karin’s in many respects. Read on to find out how the NexT Pension scheme will affect members like you.

If your situation will change by 1 January 2027, click here for the newsletter that matches your future situation. |

|

|

|

|

"My accrued pension will remain intact, and if the Fund is in good health, I may even receive something extra from the buffer." |

|

|

|

|

|

The NexT Pension scheme and your future pension |

If the finances of Philips Pensioenfonds are healthy on 1 January 2027 – assuming a 120% funding ratio for example – we expect your projected pension to immediately be higher. You will then receive a portion of the Pension Fund’s financial buffer (read more here about how this works).

We will invest your personal pension capital. The returns on those investments, together with the interest, will eventually determine what your pension is. The NexT Pension Scheme will not use a buffer like the current pension scheme does. This means that developments on the financial markets will directly affect your pension – either positively or negatively. Until you (almost)start drawing your pension, the ‘solidarity reserve’ will not offer any protection against shortfalls in the returns. Even so, the NexT Pension Scheme also has an upside: if we get off to a strong financial start and the investments yield strong returns, your pension could increase faster than it does now.

|

|

|

|

| |

|

|

|

|

From a pension entitlement to a personal pension capital |

With the NexT Pension Scheme, you will have a personal pension capital: your ‘pension savings’, made up of the contributions paid in the past and the investment returns. You will be able to see how much capital Philips Pensioenfonds has reserved for you. Important: how much pension you receive will depend on interest rates, life expectancy and investment returns. Your pension will follow economic trends, both positive and negative. Our investment policy makes allowance for these risks relative to your age. |

|

|

|

| |

|

|

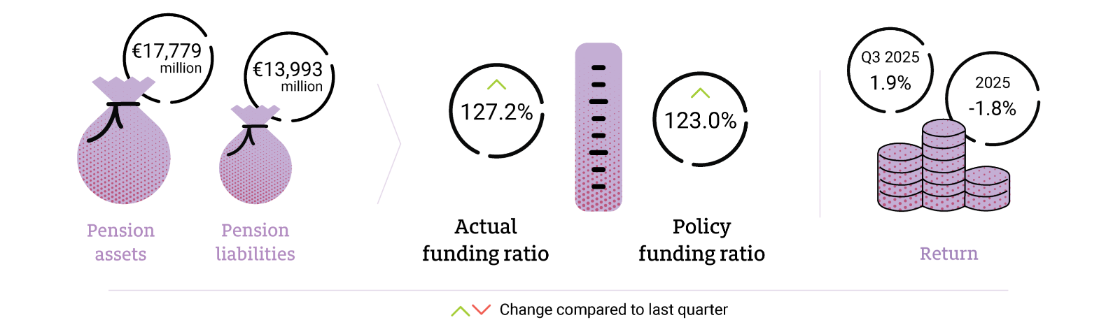

How is Philips Pensioenfonds doing? |

|

|

|

|

|

What do you think of this newsletter? |

|

|

|

| |

| |

|

|

|