News about your new pension

How will the NexT Pension scheme affect you? |

|

|

|

|

Slowly but surely we are working towards personalising the information about your new pension system: the NexT Pension scheme. Until that time, we will try to give you an idea by explaining how the NexT Pension scheme will affect people like you. This newsletter has been put together specifically for members who draw a pension from Philips Pensioenfonds.

Next week’s annual 3-day event the Pensioen3daagse will increase the country’s focus on the subject of pensions, so I believe that now is the perfect time to reach out to you. The question that you are probably most interested in is how the NexT Pension scheme will affect your own personal pension situation. We will not be able to share specific information about your personal situation until shortly before we switch to the NexT Pension scheme on 1 January 2027. For now, however, we can give you an idea of what to expect, and explain the most important matters that might be relevant in your situation. This newsletter is a key tool in these communications. Approximately midway through next year, further details about your new pension will be made available in MijnPPF. |

|

|

|

|

Anita Joosten

Managing Director |

|

|

|

| |

|

|

This is Hans. Hans is 75 and is drawing a pension from Philips Pensioenfonds. If, on 1 January 2027, you are like Hans – drawing a pension from us – then your pension situation will resemble Hans’s in many respects. What type of pension you have does not matter: whether a retirement pension or a survivor’s pension, for example. Read on to find out how the NexT Pension scheme will affect members like you. |

|

|

|

|

|

"From 2027 onwards I will receive my pension as usual, and if the Fund is healthy, I will receive a supplement from the buffer." |

|

|

|

|

|

The NexT Pension scheme and how much pension to expect |

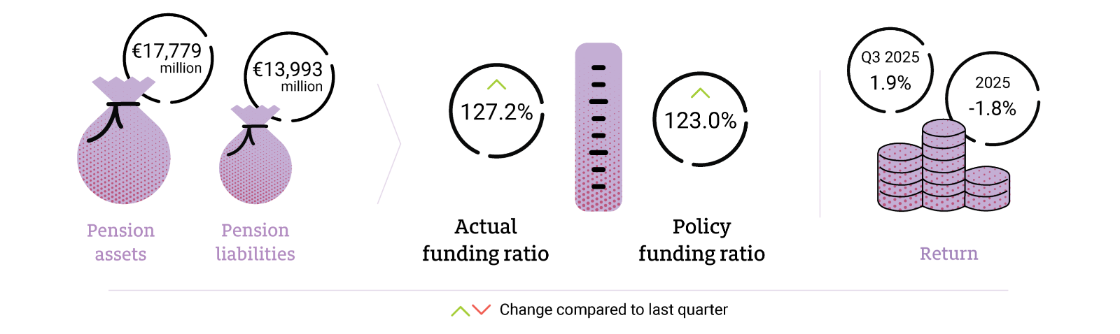

If the finances of Philips Pensioenfonds are healthy on 1 January 2027 – assuming a 120% funding ratio for example – we expect that your pension will immediately go up by about 5-8%. Looking further ahead, we expect your pension to increase by an average of about 2% per year, so it is likely to retain most of its purchasing power. The healthy starting position also means that we can top up the solidarity reserve to the full amount. That reserve is a key protection against the need to lower your pension.

Even so, some risks remain: the financial markets are unpredictable, and if the investment returns fall short, or inflation is higher than expected, your pension’s purchasing power could suffer. |

|

|

|

| |

|

|

|

|

Carrying over your accrued pension |

You will keep the pension that you have accrued before we switch to the NexT Pension scheme, and its value will become your personal pension capital when the new pension scheme takes effect. If Philips Pensioenfonds’s finances are healthy on 1 January 2027, a share in the pension fund’s financial buffer will be added to your personal pension capital, so your projected pension will go up a little right away. |

|

|

|

| |

|

|

Video: "Can my personal capital run out?" |

Even under the new system, you will still have a pension for as long as you live. If you live longer than expected, we'll continue paying your pension. Want to know how this works? Watch the video. |

|

|

|

|

|

How is Philips Pensioenfonds doing? |

|

|

|

|

|

What do you think of this newsletter? |

|

|

|

| |

| |

|

|

|