Latest developments concerning your pension fund

Latest developments concerning your pension fund Read online |

|

|

|

|

|

Your new pension is getting closer |

|

|

|

|

A new year has started, and it will be an important pension year for you and for us. We will use this year to implement the NexT Pension scheme that all our members will switch to on 1 January 2027. For you, this means that you will learn more and more about how this new pension scheme will affect your personal pension. Before that, though, this calendar quarter will be the final time that we decide on raising your pension. The outlook for increasing the pensions by indexation at 1 April 2026 are favourable: even with all the global unrest, the Pension Fund ended 2025 with a solid policy funding ratio of 125.2%. Under the NexT Pension scheme, the annual adjustment of your pension will no longer be the Board’s decision. Instead, it will be linked directly to the returns that the investments yield. This newsletter includes a link to a video in which Martin Sanders, our Investments Director, explains how your personal pension capital will be invested. We will try to achieve enough returns to ensure a proper pension, while also reducing the risks as you grow older. |

|

|

|

|

Anita Joosten

Managing Director |

|

|

|

| |

|

|

Explainer video: “How will my personal pension capital be invested?” |

|

|

|

|

|

Test your knowledge: NexT Pension |

How much do you know about the new pension scheme that will come into effect on 1 January 2027? Answer the questions below to find out! |

| |

|

|

|

|

“Why can’t I make my own investment decisions under the NexT Pension scheme? I thought the new pension system would be more individual?” |

— A question that Nicole of our Service Desk is frequently asked — |

|

|

|

|

“Management and labour have decided to adopt a solidarity-based contribution scheme. Under that scheme, individual members cannot make their own investment decisions. The pension capital is invested collectively. This means that you do not get to choose for yourself how your personal pension capital is invested. However, your returns will be apportioned by age. Younger members will receive more of the returns from investments that carry a higher risk (such as shares), while older members will receive more from the more stable investments (such as government bonds).” |

|

|

|

| |

|

|

Your pension savings & responsible investment |

|

|

|

|

-

we asked 30,000 of our members for their thoughts on responsible investment (RI)?

-

the findings will help us to align our RI policy even more closely with your priorities?

-

more than 5,000 members took part in the survey?

-

we will share the results with you during the second quarter of the year?

-

we have prepared a short animation for you to see what we are doing already in terms of RI?

|

| |

|

|

|

One of the members who responded to the survey included this urgent message: “Please keep doing your best for us, our children, our grandchildren and our great-grandchildren.” |

|

|

|

|

|

Information on indexation in March |

In the immediate future we will decide about increasing your pension at 1 April 2026. You will receive personalised information about this by the end of March. |

| |

|

|

|

|

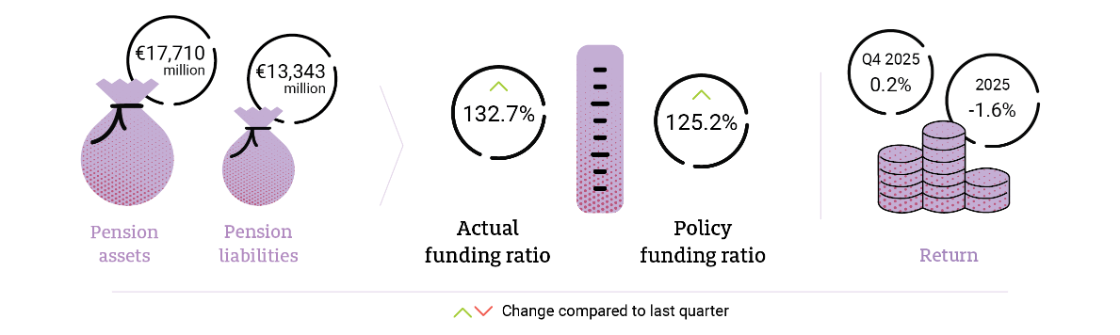

How is Philips Pensioenfonds doing? |

Strong financial position: policy funding ratio at 125.2% |

The Fund’s financial health improved during 2025. At the end of the year, we had a higher funding ratio than we did at the end of 2024, even after the full indexation at 1 April 2025. The main drivers are the higher interest rates and the financial markets’ recovery during the year after the market dip in April. The higher funding ratio means a stronger financial buffer, which is important for getting all our members off to a strong start under the NexT Pension scheme on 1 January 2027. Even so, we remain cautious. The developments around the world are difficult to predict, and that uncertainty could impact our financial position as well. We remain constantly alert to our goal of protecting the financial buffer. |

|

|

|

| |

|

|

This newsletter is intended for members of Philips Pensioenfonds who have not yet retired. Visit our website for the newsletter for members who are drawing a pension. |

|

|

|

|

|

What do you think of this newsletter? |

|

|

|

| |

| |

|

|

|