Latest developments concerning your pension fund

Latest developments concerning your pension fund Read online |

|

|

|

|

|

NexT Pension scheme: some choices revised |

|

|

|

|

As part of our preparations for the switch to the NexT Pension scheme, we recently re-examined some of our earlier decisions. Examples are the compensation system and how the financial buffer will be shared among our members. This is not something that we are doing lightly. Not only are the markets changing, we have also been talking to the Dutch central bank (DNB), as our supervisory authority. Those talks have produced new information, which we are considering carefully.

The re-examination is based on a single central premise: the Board wants the switch to be balanced, with due care for all our members. This means looking not only at the current situation, but also at extreme circumstances such as a very low – or a very high – funding ratio, and at the role of compensation for specific groups.

I believe that it is important for you to know where you stand when we switch to the NexT Pension scheme. To find out what issues played a part in the recent re-examination, visit our website. As further information becomes available, we will share it on our website and across other channels. |

|

|

|

|

Anita Joosten

Managing Director |

|

|

|

| |

|

|

Expanded scope of the compensation system |

|

|

|

|

The compensation system for the switch to the NexT Pension scheme was recently expanded. According to the latest information, more compensation should be awarded in particular to members between the ages of 30 and 50 who are accruing a pension. Nothing will change for active members below the age of 30 or above the age of 50. |

| |

|

|

|

|

Check your details in MijnPPF |

Your personal details and pension information are listed in MijnPPF. It is important to make sure that they are still up to date. For example, you should check your email address, your partner’s details to make sure that your pension is calculated correctly and that you receive important information on time. |

|

|

|

|

|

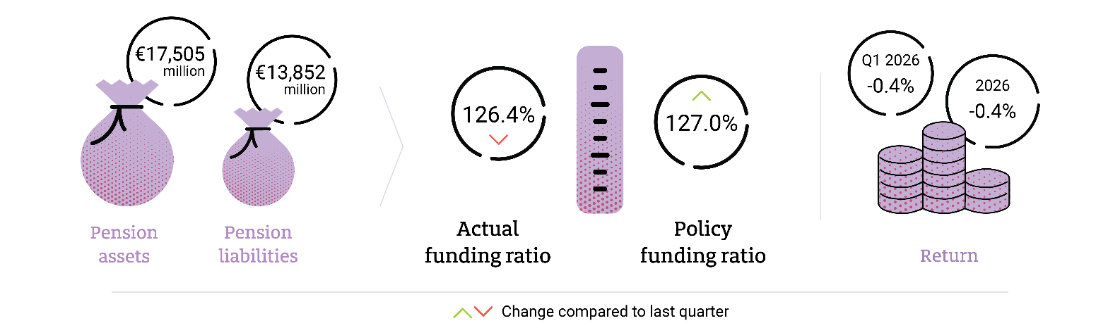

How is Philips Pensioenfonds doing? |

Pension increase affect the funding ratio |

During the last calendar quarter, the funding ratio fell by approximately 6%-points. The main cause was that the pensions were increased at 1 April 2026, which means higher pension liabilities and a drop in the funding ratio by approximately 3%-points. |

|

|

|

| |

|

|

“If I am divorced, how does this affect my pension?" |

— A question that Nidia of our Service Desk is frequently asked — |

|

|

|

|

“If you and your partner divorce or split up, this will generally have implications for your pension. For instance, your ex-partner might be entitled to part of the retirement pension that you have accrued. The survivor’s pension will also be affected: in many cases, it will become an extraordinary survivor’s pension for your former partner. What your options are and what arrangements you need to make will depend on your situation and what you agreed with your former partner. The e‑brochure ‘The end of your relationship’ provides an overview of how a divorce will affect your pension and what action you need to take.” |

|

|

|

| |

|

|

Share your thoughts: looking out for your partner after you pass away |

|

|

|

|

“I trust Philips Pensioenfonds to help with the application and payment arrangements for my partner’s pension after I am gone.” |

| |

|

|

|

|

This newsletter is intended for members of Philips Pensioenfonds who have not yet retired. Visit our website for the newsletter for members who are drawing a pension. |

|

|

|

|

|

What do you think of this newsletter? |

|

|

|

| |

| |

|

|

|